The Fed recently issued a report detailing average debit card interchange fees by payment card network. I know, it’s like Christmas in August, but try to contain your excitement. Joking aside, payment geeks like me find endless insights pouring over the details and footnotes of this annual publication. We regularly share these reports with our clients, and suggest they keep the information at their fingertips.

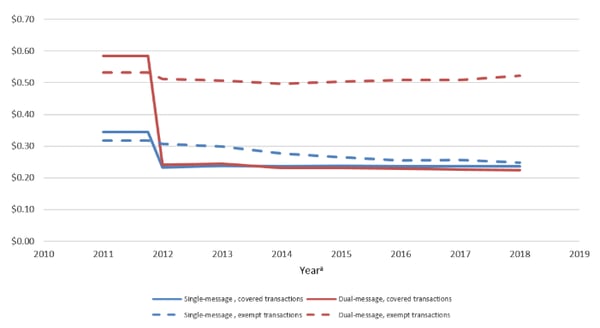

At the surface, the trend lines look pretty dull; the average interchange fee has barely budged since 2012 when the Dodd-Frank Act was enacted. Dig a bit deeper, however, and a discerning eye will notice shifts that carry major implications for the profitability of financial institutions’ card programs.

“I Must Have Put a Decimal Point in the Wrong Place or Something”

This year’s biggest news involves Discover, whose average interchange fee for signature debit transactions fell by 10 basis points in the past year, bringing it in line with MasterCard’s. (Note, we are referring to the “exempt transaction” category, for financial institutions with less than $10 billion in assets.) The interchange fee spread between Visa and MasterCard also continues to shrink, albeit much more slowly. Meanwhile, the average purchase amount for card-based transactions has ticked upward. This means that though there has been movement in basis points charge, all are seeing more value delivered to the bottom line.

This increase in purchase amount for card-based transactions, and the ongoing increase in the use of cards at the point of purchase, represents opportunity for some financial institutions. Consider that for a community bank or credit union handling 250,000 debit card transactions per month, a very small program, an improvement of just 5 cents per transaction equates to $150,000 over the course of a year. It’s reminiscent of the classic scene in the movie “Office Space” where the hapless clerk discovers that his misplaced decimal point leads to a six-figure error. It’s true, small tweaks can carry big impacts – whether through improvements to an existing program or erosion owing to a financial institution’s inaction.

The Mystic, Cryptic Language of the Card Networks

Of course, every bank or credit union’s portfolio optimization strategy, and available opportunity, will be uniquely defined based on its geographic footprint, merchant composition (for instance, are its cards most often used at big box stores or “mom and pops”), and a variety of other institution-specific factors.

There’s one strategy that stands to benefit all financial institutions, however, and it is anchored in the fact that debit cards need only include one alternative network provider. Whether through past mergers or other legacy decisions, we find that many banks and credit unions continue to enable multiple alternative networks, their numerous logos creating a visual “NASCAR effect” on the back of the card. Fewer networks mean more negotiating leverage since the institution can dangle a larger bundle of transactions to suitors. Importantly, such a move has zero impact on account holders, who see no difference in the timely processing of their transactions.

Remember, proactive contract management is essential, as network relationships can require 12-18 months’ notice prior to expiration. Once the notice is given, the real challenge comes in choosing the best network – both primary and alternative – for your institution. This is where learning to decipher “the mystic, cryptic language of the card networks,” as some of our clients have called this Fed report, comes in handy to sort through the nuances.

Last fall when the Fed released its 2016 study, we analyzed the numbers from a different perspective that remains relevant today. It might be worth a look. Information is power, and it can be used to benefit your bottom line.